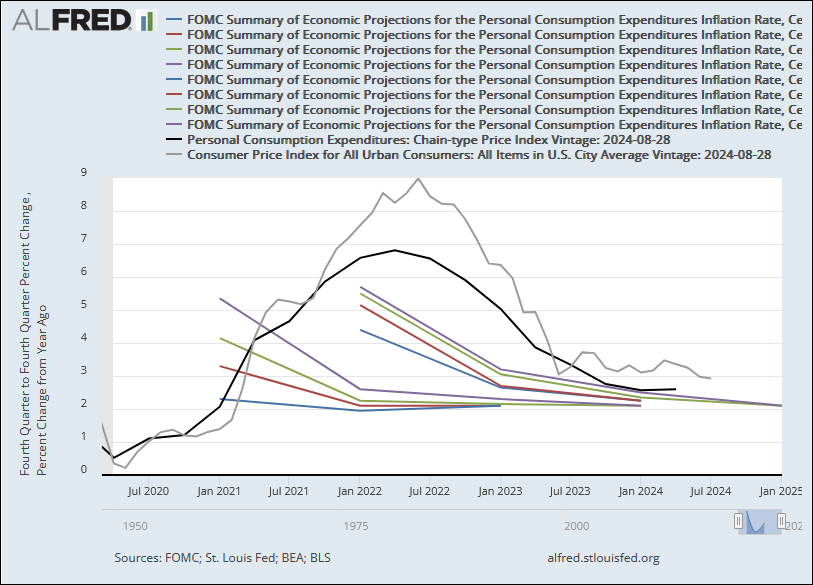

The gray line that reaches 9 percent inflation shows the CPI monthly

since March 2020, the same month the Fed reduced the interest rate to

zero to help fight covid. The black line that almost reaches 7 percent

is the PCE Price Index (FRED series PCEPI) shown at quarterly

frequency. The other 8 lines show inflation predictions made by the

Federal Open Market Committee:

|

| Graph #1: Click the image to see it bigger, or click "Graph #1" to see it at ALFRED |

The four lines that start in 2021 show the four sets of predictions made by FOMC during 2021. I'm using the same color sequence that FRED uses:

- Color 1: Blue: Here represents the March prediction set.

- Color 2: Red: Here represents the June predictions.

- Color 3: Green: Here represents the September predictions.

- Color 4: Purple: Here represents the December predictions.

The four prediction sets made during 2022 use the same colors in the same sequence.

The Fed calls them projections, not predictions. The notes explain a lot:

Projections of personal consumption expenditures (PCE) inflation rate are fourth quarter growth rates, that is, percentage changes from the fourth quarter of the prior year to the fourth quarter of the indicated year. PCE inflation rate is the percentage rates of change in the price index for personal consumption expenditures (PCEPI).

The FRED Notes identify the FRED PCEPI dataset. So I went

with that dataset for the black line on the graph above,

even though it is their monthly series. I changed the frequency to

quarterly using average aggregation; of the available options, this made the best match to FRED's quarterly series PCECTPI.

I didn't quote the whole Notes text. You can see it in the flesh at FRED or ALFRED.

Each prediction set includes 3 or 4 data values, one for the year of reporting and the rest for the following years. You'll notice that no matter the value of the first prediction, in subsequent years the predictions typically move toward the Fed's 2 percent inflation target. I suppose "projection" is a better word for this than "prediction".

The CBO does something similar when it figures Potential GDP:

CBO assumes that any gap between actual GDP and potential GDP that remains at the end of the short-term (two-year) forecast will close during the following eight years.

That's from a 20-year-old CBO paper. It may be out of date. But the methodology for both CBO and the FOMC seems to be Fret not. Things will go according to plan.

And yes, that methodology works surprisingly well in a normal economy. But when the economy downshifts from 3 percent annual growth to 2 percent annual, and there is financial crisis, and people start talking about "the new normal", well, that's when better methodology is needed.

The transcript of Jerome Powell's 17 March 2021 press conference (where he repeated his inflation warning of 4 March 2021) has Powell saying:

The median inflation projection of FOMC participants is 2.4 percent this year and declines to 2 percent next year before moving back up by the end of 2023.

That sentence has been stuck in my head since I first read it. So I dropped what I

was doing this morning when the series title "FOMC Summary of Economic

Projections for the Personal Consumption Expenditures Inflation Rate,

Central Tendency, Midpoint" turned up in FRED search results for federal spending. (Hey, I didn't put it there. I found it there!)

Looking for that Powell quote just now in the transcript, I found "FOMC" four times:

- "Today the FOMC kept interest rates near zero..."

- "... forecasts from FOMC participants for economic growth this year..."

- "FOMC participants project the unemployment rate to continue to decline..."

- "The median inflation projection of FOMC participants..."

The FOMC covers a lot of ground.

So anyway: The last of the four 2021 projections -- December -- was for 5.35% PCE inflation in the fourth quarter of 2021. FRED's PCEPI data for the fourth quarter was 5.86%. The monthly PCEPI for December 2021 was 6.18%. The monthly CPI for December 2021 was 7.18%. And the Federal Funds interest rate was zero.

The first data value from each of the 8 FOMC projection datasets on the graph is shown in this table:

| Year: | 2021 | 2022 |

| March: | 2.30 | 4.40 |

| June: | 3.3 | 5.15 |

| Sept: | 4.15 | 5.50 |

| Dec: | 5.35 | 5.7 |

Note: In the table, the first data value in the March 2021 projection is given as 2.30 percent. Jerome Powell in the 17 March 2021 transcript gives the value as "2.4 percent this year". Maybe the difference is a typo. The FOMC projection Powell describes is the same March 2021 projection presented in the table.

Every projection in 2022 was higher than the corresponding projection in 2021. And in both years, the March projection is the lowest, and each subsequent projection is higher than the one before. The Federal Open Market Committee apparently did not think inflation would go down.

It is their

job to make inflation go down. But they did not think inflation would go down. This irritates me. They were right, of course: Inflation did not go down until they started raising the interest rate. But remember, it was in March 2021 that Chairman Powell warned of inflation, and it was a year later, in March 2022, that the Federal Open Market Committee finally started raising the interest rate.

The PCE measure started coming down after Q2 2022. And the CPI measure started coming down after June 2022. In both cases, inflation was coming down since midyear. And still the FOMC projections, even the September and December projections, were for rising inflation all thru 2022. I don't understand their thought process.

It almost looks like they wanted inflation raging.

%20and%20Nominal%20GDP%20%5BFRED%201sTnQ%5D.png)

{kind=link}

{kind=link}