|

| Graph #1: Monetary interest paid: Households/Disposable Personal Income*100 |

One percent of disposable income in the late 1940s. One, one and a half percent. But there was straight-line increase to the mid-60s, followed by a much slower increase. Households already knew, then, that their debt was growing too fast.

But it wasn't that the number was getting big. It was that the cost was rising.

In the 1970s, interest rates went up a lot. The Fed was fighting inflation. Interest cost as a percent of disposable income topped out in the mid-1980s, and started slowly wandering downward. The 1991 and 2001 recessions speeded things up a bit, and the "great" recession speeded things up a lot.

It looks now like it's on the rise again.

//

The cost of interest depends on two things: It depends on the rate of interest, and on the amount of debt we pay interest on. Suppose we take out the rate of interest, and look at what remains.

I'm gonna guess that the average term of a loan is ten years. It's just a guess. Could be less. No matter.

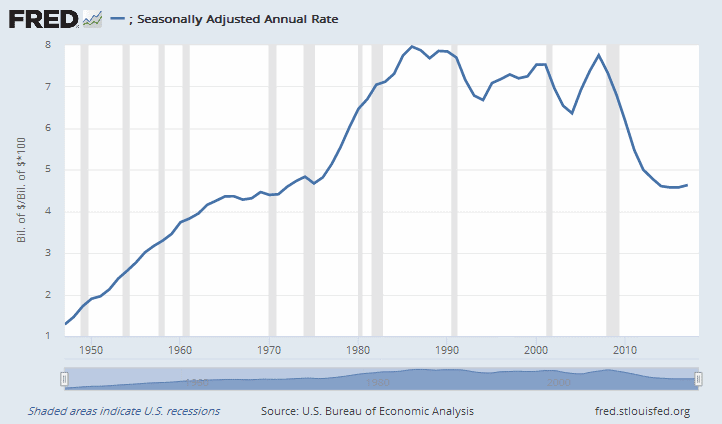

I'll take the ratio shown on the first graph and divide it by a ten-year government interest rate. There are a million different interest rates we could use; I'm using this one. Here's what I get:

|

| Graph #2: (Monetary interest paid: Households/Disposable Personal Income*100)/Long-Term Government Bond Yields: 10-year: Main (Including Benchmark) for the United States |

Look again? Down from 1963 to 1981. Up from 1981 to 2012. Possibly down after 2012, and possibly up before 1963.

Up from 1981 to 2012, reaching five, almost six times the 1981 level. Do we really need this much debt? Is the economy five or six times better now than it was in 1981? Has there been constant improvement, jiggy but constant, since 1981? I don't think so.

//

The cost of finance is like the cost of labor: It is one of the costs that contribute to the total cost of a product. The cost of finance is like the cost of productive capital that way also, except finance is not productive. It facilitates, yes, but it does not produce. But we don't need finance to do so much facilitation. We should have more government money doing more facilitation, so we would need less finance. The way things used to be.

If we cut back on finance, we can expand government money without expanding total money and without causing inflation. It would be easy, if we would do it. And by doing it, we can reduce financial cost to a practical minimum. Less debt, buddy. You love the idea.

Here's the thing. We don't need as much finance as we have. Most of finance, my guess, exists to put extra income in the pockets of the super-wealthy. A good part of it, anyway. Rent, some people call it.

We don't need as much finance as we have. We need more cash (or debit cards, if you prefer) and we need less money on which we pay interest. Maybe you think there is some problem to do that. There is no problem to do that. You just need the people in Congress and the Fed to understand the cost problem created by finance. What they see presently is the other side of that problem, the income generated by finance for themselves and their fat friends.

And I have to say no, the Democrats are no closer to understanding the cost problem than are Republicans.

No comments:

Post a Comment