In a speech given March 21, 2022, a speech ironically titled Restoring Price Stability -- on a day when the Federal Funds effective rate was 0.33 percent, and a year after he warned us inflation was coming -- Fed Chair Jerome Powell said

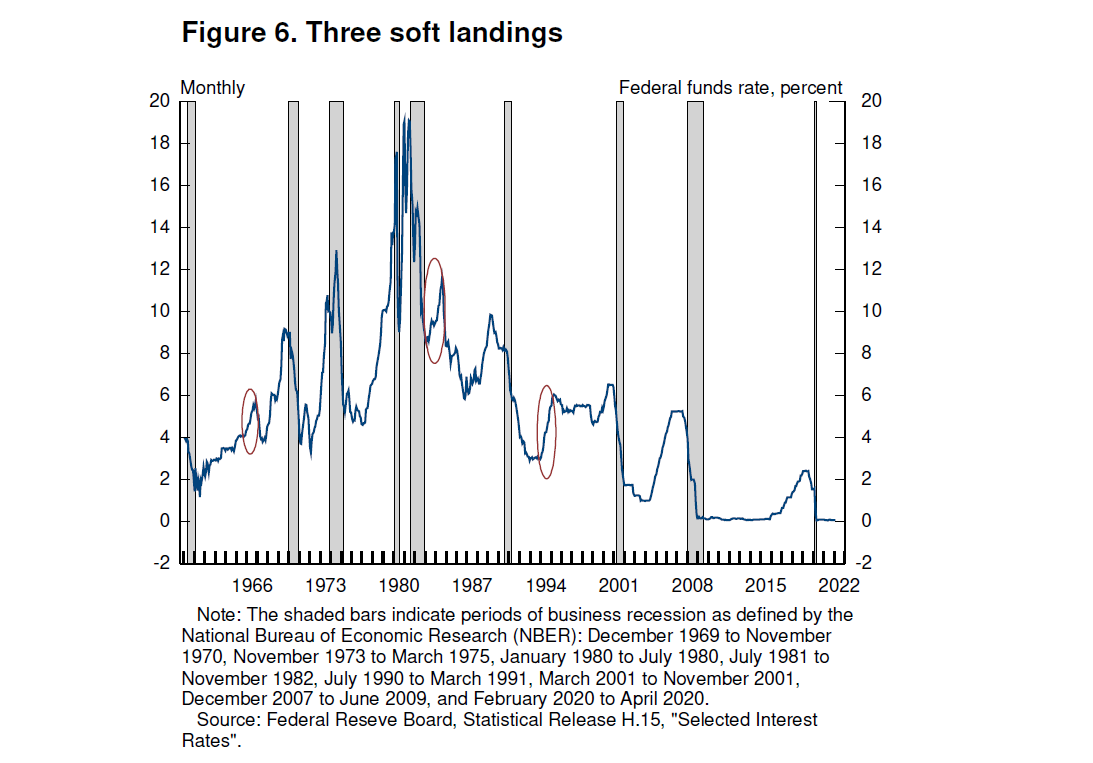

Some have argued that history stacks the odds against achieving a soft landing, and point to the 1994 episode as the only successful soft landing in the postwar period. I believe that the historical record provides some grounds for optimism: Soft, or at least soft-ish, landings have been relatively common in U.S. monetary history. In three episodes—in 1965, 1984, and 1994—the Fed raised the federal funds rate significantly in response to perceived overheating without precipitating a recession (figure 6).

Here is Powell's Figure 6:

Red ovals encircle three sharp increases in the interest rate—in 1965, 1984, and 1994. But I'm muttering to myself because Powell seems to think the interest rate shows soft landings.

My first graph below shows the interest rate that is managed by the Fed (blue), the annual rate of CPI inflation (black), and the unemployment rate (red). I show the red line a little heavier than the others, because in my view if you want a soft landing you need to watch the unemployment rate.

The Soft Landing of the mid-1960s

The graph shows January 1964 to December 1968 for https://fred.stlouisfed.org/graph/?g=1tLcA

The black line on the graph shows the rate of inflation. We don't like inflation.

The blue line (the interest rate) shows the Federal Reserve's response to inflation. The Fed increases the interest rate to fight inflation. Then, to encourage economic growth, as inflation comes down the Fed reduces the interest rate. This can be seen by noting the similarity of the black line and the blue through 1965, 1966, and 1967 on the graph.

The red line (unemployment) comes down after recession, as economic growth resumes. But over time, with growth comes inflation; with inflation comes interest-rate increase; and with interest-rate increase comes slowing growth and increasing unemployment again. You can see all these things on the graph above.

During the recovery following the 1960-61 (not shown) recession, unemployment (red) came down, inflation (black) increased, and the Federal Reserve increased the interest rate (blue) to fight inflation.

The blue (interest rate) increase -- the increase from 4 percent to nearly 6 between November 1965 and November 1966 -- is the same as the first increase circled on Jerome Powell's graph.

During that year-long interest rate increase, the decline in the red line (unemployment) came to a sudden stop in February 1966. From September through November of 1966 unemployment fell a little more, but very little. Then in December 1966 and January 1967 the rate of unemployment went up -- a warning sign of approaching recession. All this behavior was a response to the rising interest rate.

Fortunately, the black line (inflation) peaked in October 1966, and fell for several months. This allowed the Federal Reserve to reduce the interest rate. That allowed economic growth to pick up. Improving growth stopped the increase of unemployment and prevented a recession.

Since the November-1965-to-November-1966 interest rate increase did not lead to a recession, Powell describes the result as a "soft landing".

In sum, the rapid response of the Federal Reserve, lowering interest rates immediately when the rate of inflation started falling, stopped the increase of unemployment and prevented a recession. The falling interest rate saved the day.

The Soft Landing of the mid-1980s

The graph shows January 1982 to December 1986 for https://fred.stlouisfed.org/graph/?g=1tLcA

The second interest rate increase circled on Powell's graph is shown here beginning soon after the 1982 recession (the gray background): The interest rate (blue) rises from 8½ percent to almost 12.

Inflation (black) peaks near 5 percent in March 1984. The interest rate peaks five months later, in August. In 1966, inflation peaked in October and the interest rate peaked the next month. That quick response, I said, stopped unemployment from rising before it turned into recession. We didn't get such a quick response in 1984.

Fortunately, we didn't need one. As in the 1960s, in the 1980s the rising interest rate did slow the decline of unemployment. And though that decline appears to have been paused from July of 1984 to July of 1985, the rate of unemployment did not increase, and recession did not result.

Unemployment trended downward from the end of the 1982 recession to the end of the graph (December 1986). Why? Perhaps because this was the time of "Morning in America" and 1984's 7.2 percent growth of Real GDP, after what was called the "double-dip recession" of 1980 and 1981-82. Or maybe it was simply because unemployment was so high that it couldn't go higher: You would have needed a pandemic to make it go higher. Anyway, unemployment came down despite the rate of interest, and we had no recession in the mid-80s. Jerome Powell calls this one another soft landing.

The Soft Landing of the mid-1990s

The graph shows January 1993 to June 1997 for https://fred.stlouisfed.org/graph/?g=1tLcA

The interest rate -- again, blue -- increased rapidly from December 1993 to April 1995. I don't see much impact on the rate of inflation. And the rate of unemployment trended downward, without slowing, from January 1993 to March of 1995. But then, suddenly, the unemployment rate jumped from 5.4 percent to 5.8.

After that one jump, unemployment continued downward at a slower pace because interest rates were higher, but no longer rising.

Probably, if the interest rate continued rising after April 1995, unemployment would have increased also. And recession would have been in the cards.

The Squandered Opportunity of 2024

The graph shows January 2021 to August 2024 for https://fred.stlouisfed.org/graph/?g=1tLcA

Now we come to the Biden inflation.

The graph starts in January 2021, the month of Biden's inauguration. He was remarkably effective in getting that inflation started so quickly! Or I dunno, maybe he wasn't responsible for it, at all.

Anyway, in the 1960s, the interest rate peaked and fell with inflation. The falling interest rate kept unemployment from rising, and prevented a recession.

The 1980s and 1990s suggest that when the interest rate is already high, keeping it at a high level does little to push high unemployment up further. In the '90s, unemployment had to fall below 6 percent before high interest nudged it up.

A high rate of unemployment may not be pushed higher by rising interest rates. But a low rate of unemployment can be pushed higher by rising rates. In this post-pandemic recovery, since mid-2021 unemployment has been low enough that high interest rates can drive unemployment up.

The interest rate started rising (belatedly) in March 2022. CPI Inflation started falling in June 2022, and stopped falling in June 2023. The interest rate continued rising until August 2023 and remains at the August 2023 level to this day. This is not like the 1960s, when the rate of interest came down in tandem with the rate of inflation. This is more like the 1980s and 1990s, when the interest rate remained high, as if it was stuck. But our unemployment rate is low, and it is vulnerable to interest rates that are stuck at a high level. So the chances are not good that we will avoid a recession.

Sure enough, if you look for it on the graph, you can see that unemployment has been rising since early 2023. And only now, in the last couple weeks maybe, has there been any evidence of concern that we are in the process of creating a recession, with interest rates stuck at a high level to fight an inflation that has been running at about 3 percent since June of 2023.

{kind=link}